2024 Fourth Quarter Market Commentary and 2025 Outlook

Commentary

Tempered Expectations

U.S. equities delivered another solid performance in 2024, building on the strong returns of the previous year. The weight and performance of large-cap technology stocks, and the frenzy surrounding how Artificial Intelligence (AI) will transform the economy, played an important role in driving US equities higher. The Federal Reserve also deserves some credit for 2024 gains, as it successfully suppressed inflation without upending the labor market. The combination of AI trends, improving inflation metrics, and the Fed’s signal to rescind further rate increases going forward were well received by investors, and equity prices soared.

The S&P 500 finished up at 25% in 2024 with broad-based strength seen across most sectors. Atypically, both cyclical and historically defensive sectors performed well, as seen by the eleven S&P 500 Sector Indexes. Those sectors exposed to falling commodities prices were the notable laggards. Success suppressing inflation helped boost consumer sentiment during the year, benefiting both the consumer discretionary and consumer staple sectors. The excitement around AI continued to dominate tech stocks, but the technology’s power demands and the need for new data centers also propelled more historically defensive industry, such as telecom and utilities. On the weaker side of the ledger, the energy and materials sectors underperformed the rest of the market as less inflation hampers their top-line revenue growth. Despite a strong performance from GLP-1 weight loss drug companies, the healthcare sector overall also trailed. This is not too surprising as it is common for the industry’s returns to stagnate during Presidential election years due to uncertainty surrounding potential changes to the regulatory landscape.

One of the defining themes of 2024 was the Federal Reserve’s shift in policy. Following the aggressive tightening cycle of 2022 and 2023, the Fed paused its rate hikes in early 2024 as inflation continued to moderate. By the fall of 2024, with the Consumer Price Index (CPI) falling to 2.5% and marking significant progress from its 2022 peak of 9.1%, the Fed finally provided investors with the rate cuts we had eagerly awaited throughout the year. While nothing is guaranteed, continued success against inflation should enable the Fed to remove further restrictive tightening in 2025.

As we look ahead, the outlook for equities depends heavily on the continued success in managing inflation and the Federal Reserve’s ability to navigate the next phase of the economic cycle. While we appreciate the strong year for US stocks, we caution investors that 2025 may not be as lucrative as 2024. Overall, the US economy remains healthy and our blunt assessment for 2025 would simply be “more of the same”. Large-capitalization technology stocks continue to offer an unprecedented combination of profitability, return on invested capital, cash-flow generation, innovation, and growth potential. AI is still in its early stages of its proliferation and the productivity-enhancing potential is powerful. Interest rates are likely to trickle lower as the Fed unwinds the restrictive monetary conditions needed to combat inflation. Nevertheless, the stock market’s annual returns ebb and flow. Outsized return years that occur during an economic expansion tend to be followed by a period of retrenchment. Valuations today are also elevated, implying that forward returns will likely be lower. We continue to believe that owning the US companies with the strongest and most innovative leadership is the best long-term strategy, but our experience also cautions that elevated expectations, higher valuations, and underappreciated risks could limit next year’s gains. Furthermore, significant uncertainties exist in 2025 that could hamper the economy and will be digested as more information becomes available. Thus far, the market has climbed this wall of worry, but developments next year could be problematic.

The key unknown for 2025 is whether the incoming Trump administration’s campaign rhetoric will translate into tangible policy, or if it was simply red meat for voters. Specifically, can it execute meaningful plans regarding deporting immigrants, enacting tariffs, and reducing the size of the federal government. Significant logistical, practical and legal challenges exist to turn rhetoric into policy, but if realized, these are not without economic repercussions. Mass deportations threaten a return of wage inflation, similar to that which developed during the Covid-19 pandemic, when competition to attract and retain workers fueled compensation growth. Tariffs may benefit specific industries, but their costs are born by domestic consumers and a broader trade war with China, Mexico, or Canada would be economically destructive. A leaner Federal government would be more efficient, but deep public sector layoffs could increase the unemployment rate and fuel recession fears. We have no insight into the administration’s prospects or whether the rhetoric is mere negotiating bluster; only time will tell.

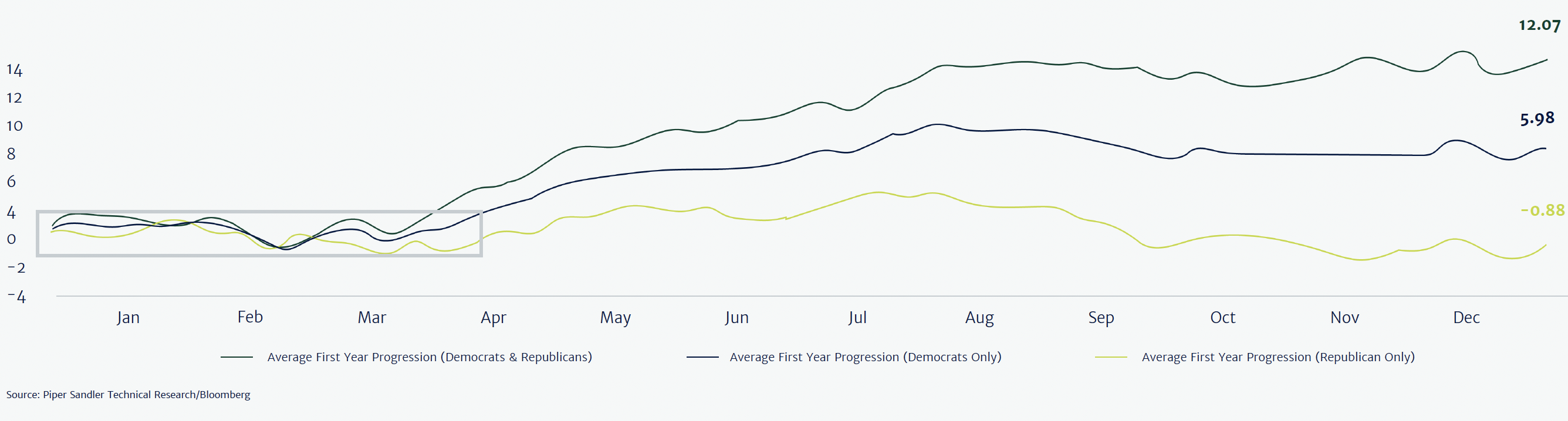

The chart below from Piper Sandler shows the stock market’s returns during the first year of a new administration. While returns under both parties in the initial months after Inauguration Day stagnate as regimes change, Republican administrations tend to underperform Democratic ones during the first year. This may be due to timing differences associated with implementing differing political priorities, such as deregulation or tax cuts that require legislation, versus increased spending or hiring that may have a more immediate impact. Regardless of the reason, the stock market during the first year of Republican administrations tends to be lackluster.

First Year of Presidential Cycle | Historical Comparison Annual Seasonality

(1928 – 2021)

Based on US Bond market’s record of an inverted yield curve, it is likely the next administration will confront a recession at some point in the future. While considered a reliable indicator historically, the yield curve’s inversion lacks precision regarding the timing of an economic contraction. Predicting recessions is notoriously foolhardy and market timing, usually leads to missing out on strong stock market returns. We prefer to adjust risk through sector exposure rather than to outright time the stock market. If anything, the un-inverting of the yield curve tends to provide a more manageable warning of a US recession, which only occurred in August 2024. With the yield curve in mind, and the uncertainty surrounding the incoming administration’s aggressive policy action that could disrupt labor markets, we do not want to be pollyannish that the past performance will always persist.

At Oak Associates, our investment philosophy remains unchanged. We favor companies with strong market positions, high levels of profitability, and disciplined balance sheets. In an environment where the cost of capital is still elevated, we believe businesses with sustainable earnings, robust margins, and shareholder-friendly practices are best positioned to deliver long-term value. The US economy remains one of the strongest and most resilient markets since the end of the Covid-19 Pandemic. As a result, US equities reflect an enviable position. While some new uncertainties have emerged due to change in Washington, the stock market is actually rather apolitical and much more focused on the economy and Fed policy than the White House. With this in mind, we remain optimistic headed into 2025 and, as always, will remain vigilant.

On behalf of everyone at Oak Associates, we thank you for investing with us.

Robert Stimpson, CFA

Chief Investment Officer

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC (Member FINRA). Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.