2022 Fourth Quarter Market Commentary

Commentary

2022 Year-End Commentary & 2023 Outlook

Happy new year. This last year has been very challenging with all of the stock market gyrations. As the market turns to a new year, rather than rehash those market movements, Oak clients have asked some common questions over the past few months which we have provided in an informational and hopefully, valuable, Q&A format for your reading pleasure. If there are additional questions, please send them and we will do our best to respond or include them in a future Q&A commentary.

Q. What are our thoughts on the overall US stock Market in 2023?

Our outlook for 2023 is non-consensus in that the first half of 2023 might be better than the second half.

We surmise that investors could expect the Fed to pause its interest rate tightening cycle, or “pivot”, and this will rescue the market from its malaise. We agree the Fed will pivot at some point, either due to inflation subsiding, a sharp recession developing, or unemployment rising. However, the pivot could coincide with weakness, may not occur decisively, or is not the Fed’s stamp of approval for a return of risk that investors anticipate. The current inflation problem did not develop overnight and we believe it will take time to get ahead of it. The Fed was slow to act and will not want to proclaim victory prematurely. Once inflation is defeated, it may be a while before the Fed returns to a more accommodative stance. Furthermore, since tightening measures take 12-18 months to permeate the economy, the full effects of the current cycle have yet to be felt. As a result, the next economic domino should be for earnings and profits to come under pressure deeper into 2023.

As we enter the new year, more evidence of progress against inflation will benefit the stock market and fuel similar “pivot optimistic” rallies that occurred during the 2022 decline. As the earnings domino arrives, it could weigh on equities but also foster the Fed’s long-awaited pivot.

Q. Has the market bottomed yet?

Bottoming is a process. We anticipate the current tightening cycle will result in a more protracted recovery, rather than the V-shaped bottoms of the past, as investors patiently await the Fed’s heavy-handedness. A protracted recovery is more probable due to the limited monetary tools available following the demise of quantitative easing and recent inflation. These intervention tools are inflationary and likely unusable in the current economic environment. While valuations have reset and we are optimistic about the next bull market, there remains a significant amount of interest rate tightening and constraints impacting the economy. Friction in the labor market is also not easily resolved due to changes in the labor force and lingering effects of the pandemic.

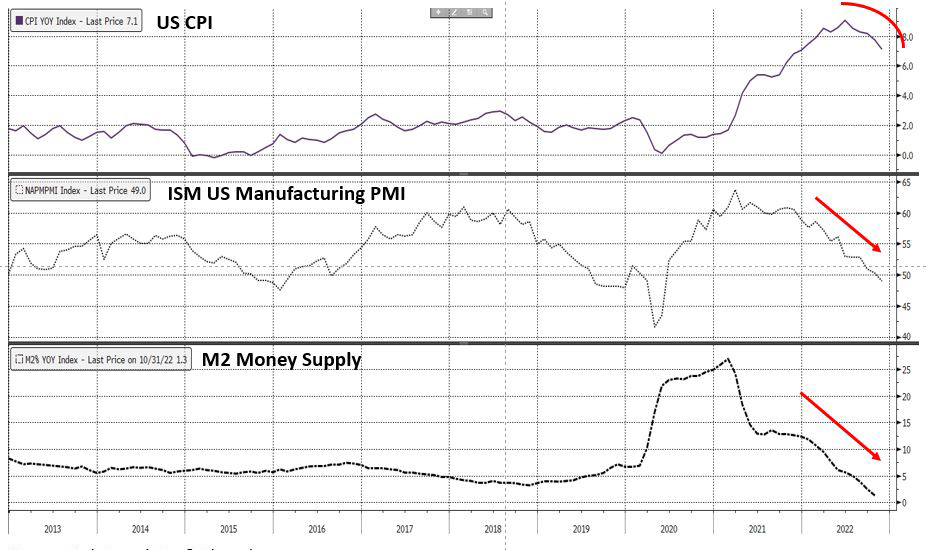

Fortunately, we find the Fed’s actions are going to plan. The chart below shows inflation (via the CPI), economic activity (the PMI Index), and the Money Supply (M2). Inflation (top line) is rolling over, led by a more rapid decline in economic activity (middle) and starvation of the money supply (bottom). This increases our confidence that inflation is being contained.

Source: Oak Associates & Bloomberg

Q. Large-Cap Tech was among the hardest hit in 2022, is the segment irreparably damaged?

In short, no. Not all tech companies are created equal. There is also a wide dispersion in quality and profitability across tech. Some of the elevated weakness in mega-cap tech was the result of prior multi-year outperformance, being included in the unwinding of the work-from-home trade, and idiosyncratic issues at specific companies. High-flyers that exhibited persistent astronomic valuations may struggle to reclaim their fan base. However, the long-term opportunity for blue-chip tech leaders has not changed and they are now trading at reset valuations.

That said, some areas of the market have benefited from the more than two decades of loose monetary conditions and the risk appetite that tolerated deferred profitability and rapid growth. Oak has always preferred quality growth businesses and companies which respect shareholder capital. With diligence, a unique combination of profitability, growth, and innovation at attractive valuations still exists in technology stocks. These characteristics are likely to become more valuable now that the unlimited access to low cost funding, whether through the capital markets, venture capital, or private equity, is both constrained and more discerning.

Q. Healthcare was a top pick for 2022, what about 2023?

Healthcare stocks continue to present an attractive combination of valuation, counter-cyclical characteristics, demographic trends, and a still unfolding return-to-normal. The sector’s performance last year has shifted the risk/reward for some industries within healthcare, and we may make changes as needed. Outside of healthcare, relative valuations in areas of technology and defense/industrials are also appealing. Historically defensive sectors, such as utilities and staples, are trading at elevated valuation levels.

Q. Energy outperformed in 2022, is it a new growth sector?

Energy’s outperformance was driven by the combination of inflation, record profitability following the pandemic, and disruption in the global energy market caused by the war in Ukraine. The sustainability of these factors remains uncertain. This is also not the first time the energy sector has been suggested as a new growth industry, such as peak oil or the shale era of the mid-2000s. Nevertheless, we will continue to assess the sector and the long-term opportunity, cognizant of its highly-cyclical nature, regulatory issues, and competitive threats.

Q. When will inflation return to 2%?

We do not anticipate a rapid return to a 2% inflation backdrop due to changes in the labor force and pandemic-related shifts in the global supply chain. Nevertheless, the economy has functioned quite happily with inflation between 2-4% historically and lower inflation isn’t necessarily optimal. Most economists agree, some inflation is beneficial. More important to investors however, is the market’s behavior following periods of high inflation.

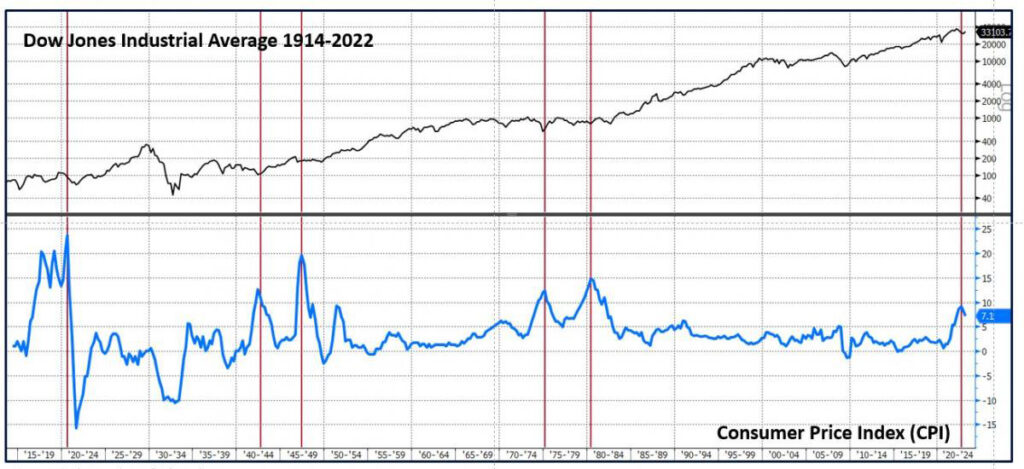

Source: Oak Associates & Bloomberg

The chart above shows the Dow Jones Industrial Average since 1914 with the CPI Index as a measure of inflation. The century-long chart obscures the precise timing of turns in the data, but the inferences are clear. Once inflation has peaked, the market tends to bottom and embark on its next bull run. As noted in the previous chart, the inflation fire is being starved of both fuel and oxygen. While this hampered equities in 2022, the strategy is working and solving the inflation problem is a long-term positive for consumers and investors.

Final Thoughts

Predicting the path of the short-term equity market is often foolhardy. We prefer to shape the portfolio for the environment we anticipate and respond as the situation changes. It is likely the US will notch a recession in the future, as predicted by the yield curve and due to the tremendous amount of friction injected into the economy by credit markets and the Federal Reserve. The stock market’s 2022 decline discounts this outlook and as mentioned, bottoming is a process. For the long-term investor, the future remains bright.

Thank you for your investment with Oak Associates.

Wishing all of our clients a happy new year. Thank you for your investment with Oak Associates.

Robert Stimpson, CFA

Co-Chief Investment Officer

Oak Associates, ltd.

To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

IMPORTANT INFORMATION

The statements and opinions expressed are those of the author and do not represent the opinions of Oak Associates or Ultimus Fund Distributors, LLC. All information is historical and not indicative of future results and is subject to change. Readers should not assume that an investment in the securities mentioned was profitable or would be profitable in the future. This information is not a recommendation to buy or sell. This manager commentary represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice.

Past performance is no guarantee of future results. Investments are subject to market fluctuations, and a fund’s share price can fall because of weakness in the broad market, a particular industry, or a specific holding. The investment return and principal value of an investment will fluctuate so that an Investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Click here for standardized performance.

The S&P 500 Index is a commonly-recognized, market capitalization-weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance. One cannot invest directly in an index.

CFA is a registered trademark of the CFA Institute.

Oak Associates Funds are distributed by Ultimus Funds Distributors, LLC. Ultimus Fund Distributors, LLC and Oak Associates Funds are separate and unaffiliated.

16238467-UFD-01/06/2023