Building Generational Relationships for the Great Wealth Transfer

Advisor Resources

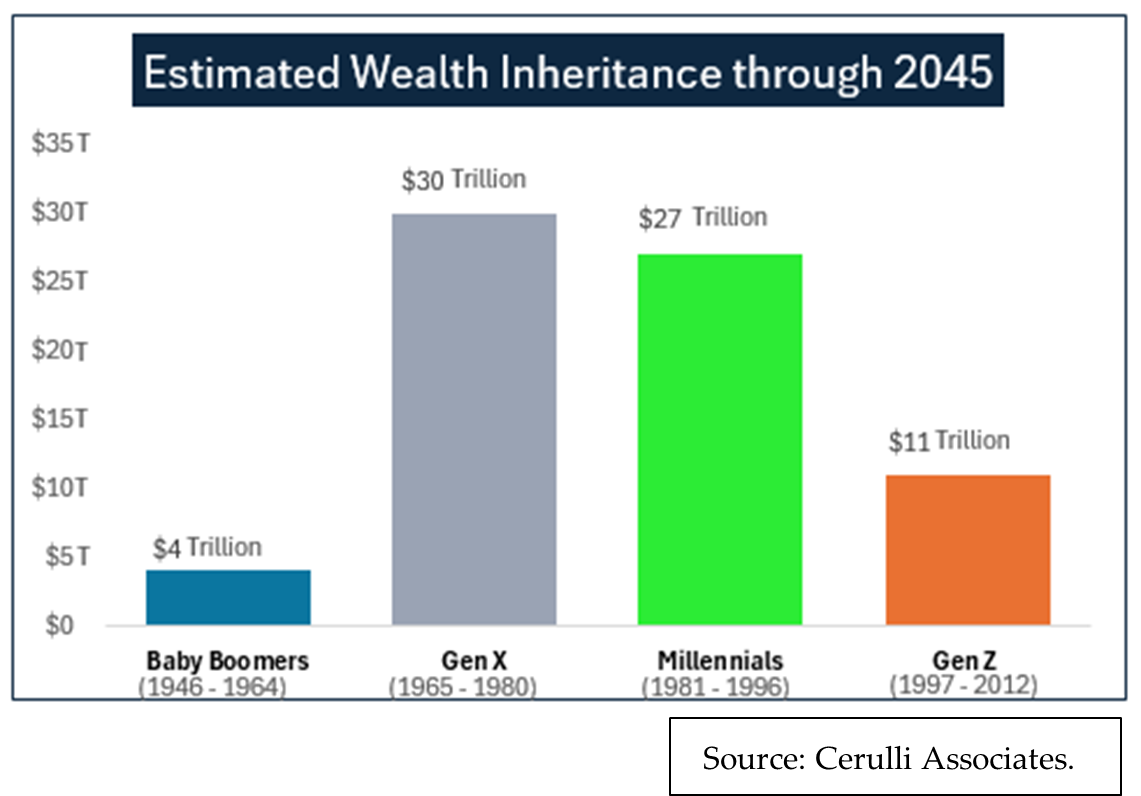

The great wealth transfer, wherein baby boomers will pass trillions of dollars to their heirs both during their lifetimes and as inheritances afterward, is already underway and will continue for another 20 years or so. Estimates of the amount to be passed down to Gen X, millennials and Gen Z vary, but most studies agree it will be between $80 and $90 trillion.1 This largest wealth transfer in history presents both a challenge and an opportunity for advisors, but what is certain is that if you don’t develop strong relationships with your current clients’ heirs now, the chances of retaining assets are low.

Magnitude of the Great Wealth Transfer. With all 76 million baby boomers (born 1946 to 1964) turning at least 65 by 2030 and owning more than 50% of the personal wealth in the U.S., researchers expect a great generational transfer of assets that equals more than five times the amount of assets held by the 2,668 wealthiest people on the planet.2 Approximately $72 trillion is expected to go to next-generation family members and the rest to charity.3 Notably, about 68% of the wealth transferred between 2020 and 2045 will come from households with at least $1 million in investable assets,3 a segment many of your clients fit into. It also means 32% of the wealth transferred will come from households with less than that, promising great opportunity.

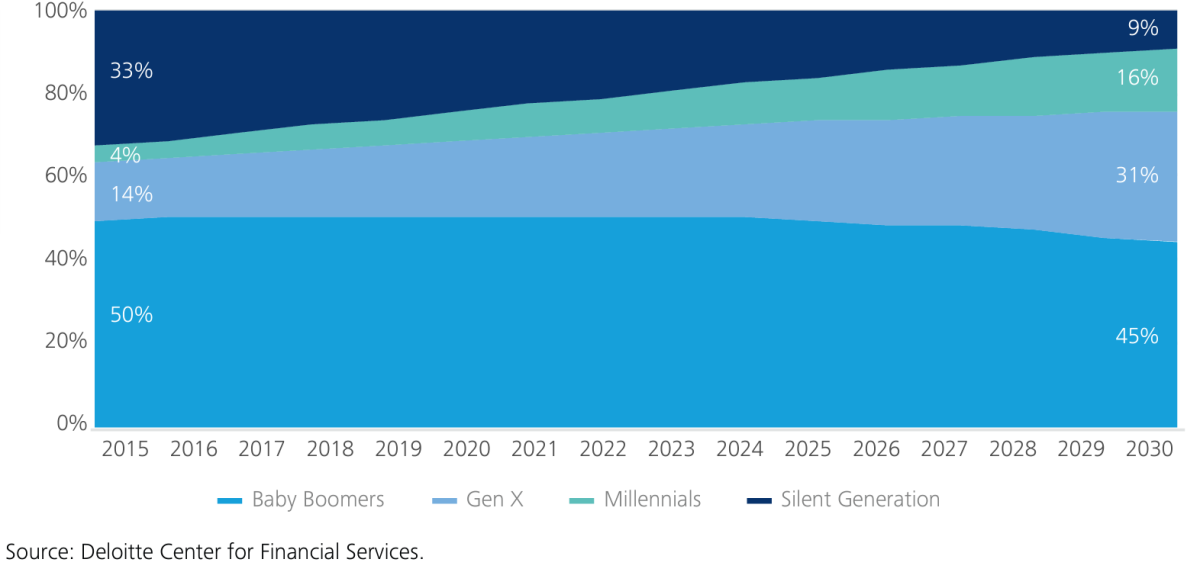

Opportunities for Proactive Advisors. Currently, nearly half of all Americans plan to leave an inheritance, but more than one-third of American families do not plan on discussing with their families how their assets will be transferred to the next generations.4 Further, only about 25% of adults feel prepared and confident in the process of how best to pass on inheritances. The opportunity for proactive advisors is that 57% of Americans believe having a financial professional guide to inform their family discussions around wealth transfer and inheritance would make planning easier.5 More than 70% of Gen Z and millennials agree there are financial topics they want advice on but aren’t sure how to get it.6 As seen to the left, the estimated changes in generational share of net household wealth ownership will already show significant shifts by 2030.7 The risk of not building generational relationships now is that 80-90% of heirs will look to change financial advisors once the inheritance is complete.8

Strategies to Build Generational Continuity and Enhance Asset Retention Opportunities

The wealth transfer process can be complicated, both for those transferring their wealth and for the heirs receiving it. But there are several ways you can turn heirs into clients. Overall, it means serving as the bridge between your clients and the people inheriting their wealth in order to deepen your existing relationships, put future generations on a solid financial path and retain assets on your book long after a client’s passing. It will take patience, time, understanding, active deliberate engagement and a willingness to evolve. Trust is key. Action is essential.

Get to Know Your Clients’ Families Now. Set up a family meeting. Encourage open communication about expectations with the intention of determining what matters most and managing family dynamics and financial complexity. Talking about the transfer process offers a meaningful way to reinforce family values and redefine family goals. Get a feel both for your clients’ heirs financial life stage, which is far more important than their chronological age, as well as for their curiosity level around building and protecting wealth.

- Ask your current clients to visualize their legacy.

- Recognize the unique needs, aspirations, interests and concerns of each individual.

- Find out about the heirs’ marriage status, children, career and any special needs.

- Approach conversations with empathy and a personalized approach.

Cultivating intergenerational relationships is all part of being a forward-thinking, strategic advisor and positioning yourself to capture—with a long-game perspective—what is today a major untapped market.

Help Create a Customized, Comprehensive and Documented Transfer Plan. Your current clients trust you to help protect their wealth, giving you a significant advantage in this transfer. Talk to them about different kinds of trusts. Discuss the option of giving while living. Help them prepare for the inevitable and mitigate potential negative consequences later not only through a will but through an estate plan. Consider ways to preserve wealth and minimize taxes. Create contingencies to address unforeseen events. Based on everything you have learned at the family meeting, make sure the plan you help create reflects and empowers each generation’s wants and wishes, aligns visions and values, and balances the needs of family members. Then, once established, make sure the heirs know where to find all relevant documentation.

Be Accessible and Indispensable to the Younger Generation. A trusted adviser can provide value-added guidance, act as an accountability partner and offer an unemotional perspective on financial decisions. Take a holistic approach, acting more as a financial coach to provide them with pro bono advice that addresses different facets of their financial lives, such as tax planning, student loan management, saving strategies and estate planning—now, before they even inherit any assets.

- Tell success stories to illustrate how your strategies have worked effectively in real-life scenarios.

- Demonstrate your expertise.

- Reassure them of your capabilities.

- Show a sincere commitment to their financial well-being.

{kind=link}

By fostering trust now, you are providing the younger generation with the building blocks they need to turn to you in the future

Communicate Regularly and with Transparency. The hard part is capturing the attention of the next generations. Keep adult children in the loop on updates and be honest about risks to the amount your clients believe they may have to pass on. For example, for many, ballooning health care and long-term care expenses will claim a chunk of retirement savings. And recognize that with people living longer, the wealth transfer conversation needs to be a dynamic, ongoing and oft-repeated dialogue. The quarterly outreach to which many advisors are accustomed is not enough. Younger generations live in a world of endless new content, wherein more is more. But make sure your communications are collaborative as well as relevant and tailored to them. Your objective is to establish meaningful connections.

Update Your Technology and Engagement Methods. You want to make sure every interaction resonates with the younger generation, who are digital-first in almost every area of their lives, including financial. So how you communicate with and deliver value to them must match this. Make sure there are platforms available that make it easy for them to access and manage data and documents. At the same time, don’t underestimate human engagement.

Maintain a professional social media presence to stay connected.

- Sponsor or host family-oriented events, such as a movie night, and young adult gatherings, such as a sports outing, and make sure you are there to mingle.

- Keep track of heirs’ birthdays, anniversaries, graduation dates, growing families and more—and snail-mail personally-signed cards along with small occasion-appropriate branded gifts for these special days.

Recognize Younger Generations’ Mindsets. Many younger adults have been unable to hit the same milestones as their parents. After all, they have had to contend with, among other headwinds, an explosion in student debt, rising inflation, the Great Recession of 2008, high mortgage rates and the COVID-19 pandemic—all while at still-developing stages of their lives and careers. Their perceptions of money may be different than their parents. They may wish to expand beyond a traditional stock, bond and real estate portfolio with interest in alternative investment opportunities that represent their personal values, favored causes and ESG criteria.

Educate Heirs on Financial Issues. There is a responsibility of stewardship with wealth, and so it is your responsibility—and growth opportunity—to help enhance financial literacy, offering your clients peace of mind and ensuring heirs are better prepared to manage, preserve, and grow their inheritance responsibly.

Helping heirs now navigate practical and thoughtful financial planning for their futures will be critical to making the coming wealth transfer more seamless.

- Send your clients’ heirs jargon-free resources about investment basics, saving for college, home buying, social security benefits, estate planning and more.

- Host legacy-focused seminars, webinars or workshops tailored to the concerns and interests of this demographic and personally invite your clients’ adult children.

- Serve as the network hub for a team of experts, such as tax preparers and insurance providers.

{kind=link}

Interested in More Info?

For questions or to speak with the Oak Associates Funds’ Relationship Manager, contact Sarah Hill at 330-819-3308 or shill@oakassociates.com.

Check out our News & Commentary at oakfunds.com for updates on the Oak Associates Funds.

For mutual fund information, call today: 1-888-462-5386 or visit our website at www.oakfunds.com

Sources

1 Cerulli Associates; Knight Frank.

2 Forbes.

3 Cerulli Associates.

4 Edward Jones.

5 NEXT360 Partners.

6 intelliflo.

7 Proactive Advisor Magazine.

8 Edge Partners, ReachStack, SS&C Advent.

Past performance is no guarantee of future results. Oak Associates Funds are available to U.S. investors only. The thoughts and opinions expressed in the article are solely those of the author as of August 15, 2023. To determine if the Oak Associates Funds are an appropriate investment for you, carefully consider each Fund’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the Funds’ prospectus, which may be obtained from your investment representative or by calling 888.462.5386. Please read it carefully before you invest or send money.

Portfolio holdings are subject to change and should not be considered investment advice. The portfolio holding information is as of 6/30/2024. Red Oak Technology Select Fund Top 10 holdings as a percent of assets were: Alphabet 10.23%, Amazon 7.48%, KLA Corp 7.35%, Microsoft 6.54%, Synopsys 5.77%, Oracle 5.45%, NVIDIA 5.45%, Meta 5.43%, NXP Semiconductors 4.49% and Qualcomm 4.49%.